The Market Crashed 45%. The Infrastructure Didn't Notice.

Perception Weekly - February 16, 2026

The most telling number from last week is the gap between what financial media said and what crypto media said, and what each audience did about it.

Bloomberg and CNBC published 74 articles about digital assets last week. 35% percent of them were negative.

"Crypto Winter," "liquidation spiral," "50% plunge." CNBC actually aired a segment asking whether Bitcoin's "purpose" needs to be questioned.

Meanwhile, CoinDesk and The Block published 75 articles. Only 19% were negative. The rest covered BlackRock listing BUIDL on Uniswap, Hong Kong greenlighting perpetual contracts, JPMorgan publishing a bullish 2026 outlook, and Ark Invest buying Bullish stock for the tenth consecutive day.

Same week. Same market. Completely different stories being told.

The Gap Last Week

The divergence: 23.5 percentage points. Financial media ran 42% negative coverage last week. Crypto media ran 19% negative. That's the widest gap we've measured in the Feb 9-16 window.

Context: The Perception Index averaged 39.9 the week before (Feb 2-9), bottoming at 34.71 when BTC plunged to $60,033 on Feb 5. At one point, the index touched 9, the lowest reading since 2019.

Last week it recovered to an average of 46.7, briefly crossing into neutral territory (51.13) on Wednesday before settling around 43 to 46.

What this means: The Bloomberg terminal crowd is pricing in continuation risk.

StanChart slashed their BTC target to $100K and warned of a slide to $50K. Coinbase got cut to sell. The word "capitulation" is showing up in headlines.

But the builder audience, the people at Consensus Hong Kong, is watching BlackRock make its first DeFi move, Hong Kong issuing stablecoin licenses, and $18.8 trillion in household debt that constrains how long the Fed can stay restrictive.

When the narrative diverges this hard, historically one side is wrong. Last week's data suggests it might not be the builders.

Narratives in Motion

ACCELERATING: "Not a Crypto Crisis"

114 articles on the crash. 53 on extreme fear. 118 on exchange flows. But the framing is shifting.

Multiple panels at Consensus Hong Kong explicitly called this "a TradFi event, not a crypto crisis." Abraxas Capital's Fabio Frontini pointed to the yen carry trade unwinding, the same mechanism that roiled global markets in August 2024 when Japan's surprise rate hike forced leveraged positions across asset classes to unwind.

The dominant explanation has pivoted from "crypto is broken" to "macro broke everything and crypto was the most liquid collateral to sell." This reframing matters because it implies the recovery doesn't need crypto-specific catalysts. It needs macro relief.

What to watch: January CPI came in at 2.4% YoY, slightly below expectations, pushing BTC back to $70K last Friday. The next inflection point is the February FOMC minutes on Wednesday, Feb 19. Any signal toward cuts and the "this was just macro" thesis gets its confirmation trade.

For PR teams: The "not a crypto crisis" frame has 2-3 more weeks of runway. If your company is building infrastructure, this is the window to push that narrative while it still has momentum.

For analysts: Track the gap between CME futures premium (bullish Wall Street positioning) and offshore exchange discount (bearish retail positioning). When these converge, it tends to signal a directional move.

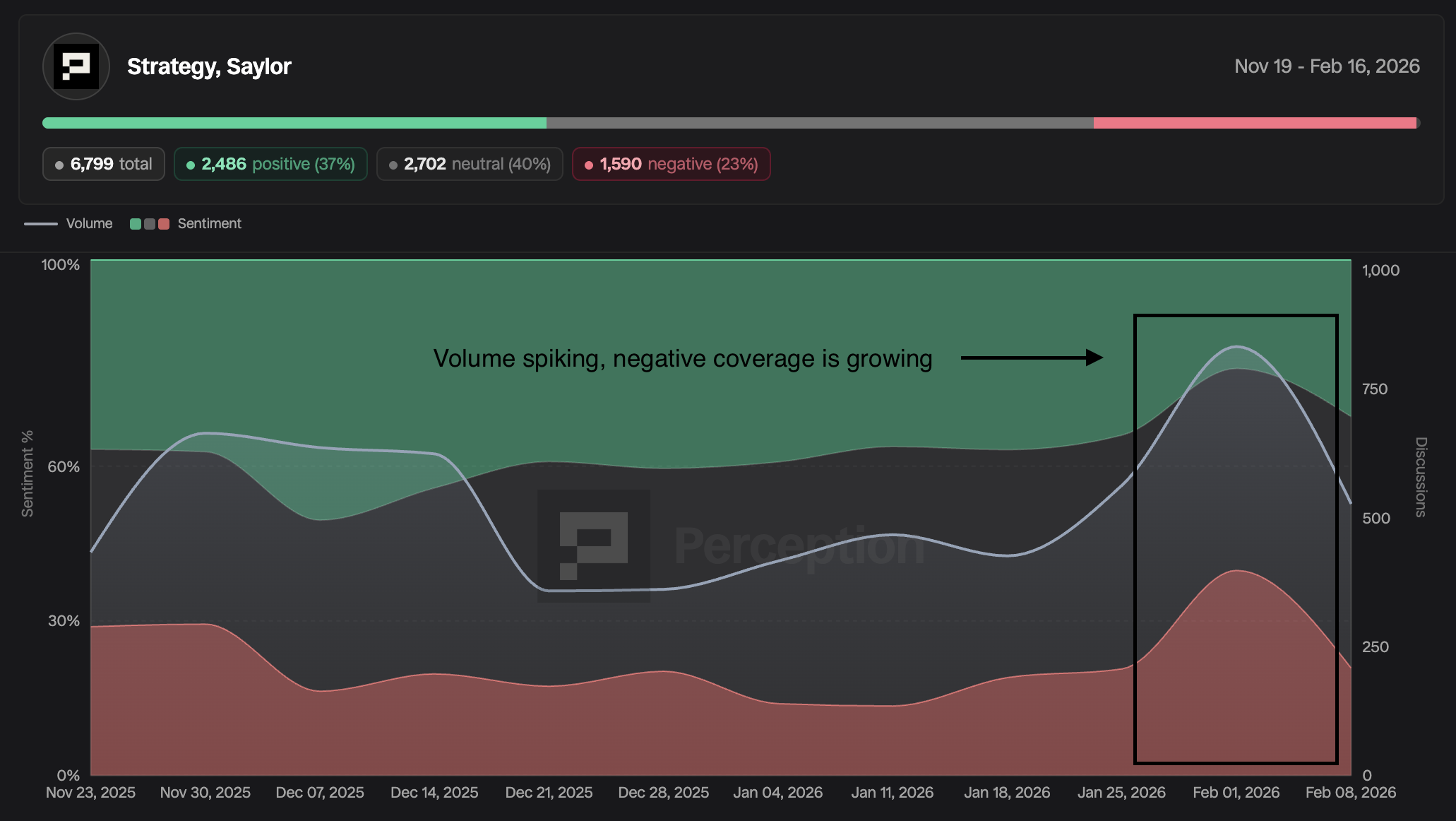

PEAKING: Strategy/Saylor Accumulation

93 combined articles last week. Strategy bought 1,142 BTC for $90M at roughly $78,815 average. Total holdings: 714,644 BTC. Saylor went on CNBC to say he'd buy "every quarter forever" and would "refinance the debt" even if BTC fell 90%.

Meanwhile, Strategy's stock rebounded 33% from its Feb 5 low, suggesting the equity market is more confident in the BTC accumulation thesis than the crypto market is in BTC itself.

Here's the signal that this narrative is peaking: when Saylor has to publicly deny forced selling, the coverage has moved from offense to defense. The 10-K showing total holdings below cost basis is the detail the bears keep circling.

Bernstein reiterated their $150K target and called this the "weakest bear case in history" but 25.6% of coverage was negative.

That's high for a narrative that was almost entirely bullish two months ago.

What to watch: Strategy's next 8-K filing.

If they announce another purchase in the $60K to $70K range, well below their average, it confirms dollar-cost averaging through a bear market.

If they skip a quarter, the narrative changes entirely.

EMERGING: The Institutional Infrastructure Build

Five signals converging last week:

Peter Thiel and Palmer Luckey launched Erebor, a $4B Bitcoin-inclusive startup that secured an OCC bank charter. BlackRock listed BUIDL (tokenized Treasuries) on Uniswap, their first DeFi move. Hong Kong approved crypto margin financing, perpetual contracts, and stablecoin licenses for March. JPMorgan published a note saying they're "positive on crypto for 2026, led by institutional investors."

While price action grabbed headlines, the institutional plumbing got a major upgrade last week. BlackRock doing anything in DeFi is a Rubicon moment. Thiel getting an OCC charter for a Bitcoin-inclusive bank is new ground.

What to watch: BlackRock's Nicholas Peach said a 1% portfolio allocation to crypto across Asia could unlock $2 trillion in new flows. Aspirational, but the fact that a BlackRock executive is publicly sizing that number tells you where their product roadmap is headed.

For BD teams: The ICE and Hong Kong developments open regulatory doors. If you're scoping expansion into Asian markets or traditional finance partnerships, the window is forming now, not next quarter.

DORMANT: Stablecoin Regulation

The GENIUS Act was the hottest topic in January. Last week, it barely registered. A White House meeting between banks and crypto companies ended in impasse. Banks are demanding zero stablecoin yields. Crypto companies are pushing back.

Reuters called the banks' position "flawed." The Block reported the bill's 2026 fate "hinges on Trump and stablecoin yields."

The legislation stalled, but the infrastructure didn't wait. MoonPay launched stablecoin payroll. Agant received FCA registration for a GBP stablecoin. Stablecoin market cap rose 50% after the GENIUS Act passed, per Binance's Richard Teng.

What to watch: Whether Trump personally intervenes in the yield impasse. If the bill stalls into Q2, the window for 2026 passage narrows considerably.

The Prediction

Bitcoin will close February above $72,000.

Confidence: Medium.

Three supporting patterns.

First, sentiment has bottomed and is recovering.

The Perception Index's single-digit reading is historically a contrarian buy signal.

When the index last hit that level, BTC rallied 40%+ in the following 60 days.

Second, institutional buyers are accumulating, not retreating: whales moved $4.7B to cold storage while retail panic-sold, Binance converted its $1B SAFU to Bitcoin, and CME futures still show a premium even as offshore exchanges show discount.

Third, the macro backdrop improved. January CPI at 2.4% (below forecast) and strong jobs data (130K vs. 70K expected, unemployment down to 4.3%) give the Fed more room while keeping rate-cut hopes alive.

What would invalidate this: A second leg down from tariff escalation, surprise hot CPI, or Fed hawkishness. A contagion event spreading beyond smaller platforms. Or Strategy disclosing material adverse conditions on their BTC position.

The Close

Willy Woo posted yesterday: quantitatively speaking, the bottom is far from in.

He's looking at old whale wallets from the Satoshi era selling over the past 12 months and sees capital flows that suggest more downside.

Samson Mow's response framed the fear itself as the trade, arguing that selling into quantum computing concerns would prove to be a transfer of BTC from the fearful to the patient.

Two people looking at the same market. One sees the flow of old coins as a leading indicator of structural change. The other dismisses fear as the opportunity.

The data last week suggests both are partially right.

The on-chain flows are real: 50,773 BTC to exchanges in 15 days. But the institutional infrastructure buildout is also real: OCC charters, BlackRock in DeFi, ICE futures contracts.

The question isn't about price anymore. It's about whether this market is consolidating before its next move, or consolidating before a structural change in who owns what and why.

The answer probably isn't in the charts. It's in the 13-F filings that drop next quarter.

See you next Monday.

-- Fernando

Built on Perception's analysis of 450+ curated media sources, real-time trend intelligence, and sentiment tracking for the week of February 9-16, 2026. BTC price at time of writing: $68,706.

If you want to see what I'm seeing in real-time → perception.to